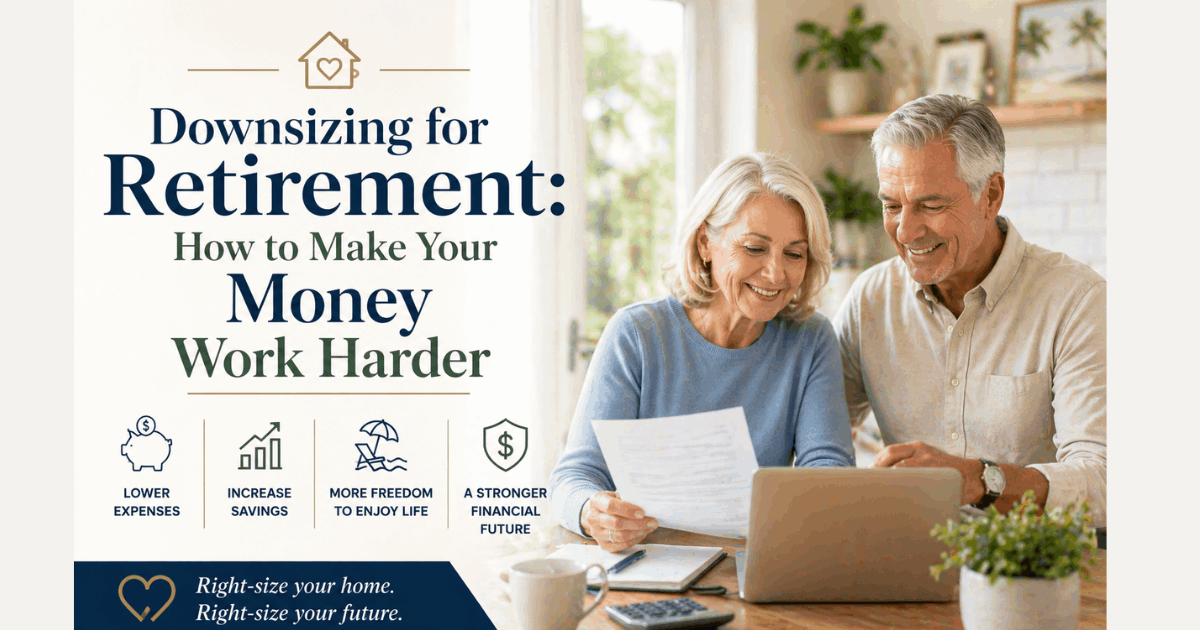

Retirement is one of life's most anticipated milestones — a time to travel, pursue passions, and enjoy the fruits of decades of hard work. But making the most of retirement often requires smart financial decisions, and one of the most impactful is downsizing your home. For many retirees and pre-retirees, their largest asset is the equity locked up in their house. Downsizing strategically can transform that equity into lasting financial freedom.

Retirement is one of life's most anticipated milestones — a time to travel, pursue passions, and enjoy the fruits of decades of hard work. But making the most of retirement often requires smart financial decisions, and one of the most impactful is downsizing your home. For many retirees and pre-retirees, their largest asset is the equity locked up in their house. Downsizing strategically can transform that equity into lasting financial freedom.FROM OUR BLOG

How to Sell Your Home Fast in Fort Lauderdale: Expert Tips from PREMIERE Group

Selling Your Home in Fort Lauderdale: What You Need to Know in 2026 Selling a home in Fort Lauderdale's competitive real estate market requires the right strategy, the right pricing, and the right agent. Whether you are selling a waterfront estate in Las Olas Isles or a family home in Weston, PREMIE

Living in Weston, FL: The Complete Real Estate Guide for 2026

Why Weston, FL Is One of Florida's Most Desirable Cities to Live Nestled in Broward County just west of Fort Lauderdale, Weston, FL has earned its reputation as one of the most sought-after communities in all of South Florida. With master-planned neighborhoods, top-rated schools, a low crime rate, a

Top Luxury Homes for Sale in Fort Lauderdale, FL: 2026 Buyer's Guide

Why Fort Lauderdale Is the #1 Luxury Real Estate Market in South Florida Fort Lauderdale has long been celebrated as one of South Florida's premier destinations for luxury real estate. With stunning waterfront properties, world-class dining, top-rated schools, and proximity to Miami, Fort Lauderdale